APEC at a Crossroads: Resilience Under Pressure

The APEC region enters 2026 with short-term resilience intact, but the outlook is increasingly clouded by intensifying geopolitical tensions and supply disruptions. The ongoing crisis around the Strait of Hormuz, a critical artery for global flows of oil, gas and by-products, has sharply raised energy prices and production costs and heightened uncertainty.

These developments are beginning to weigh on demand, trade and production across the region, exposing fragilities beneath otherwise steady growth.

Multiple shocks dim growth prospects

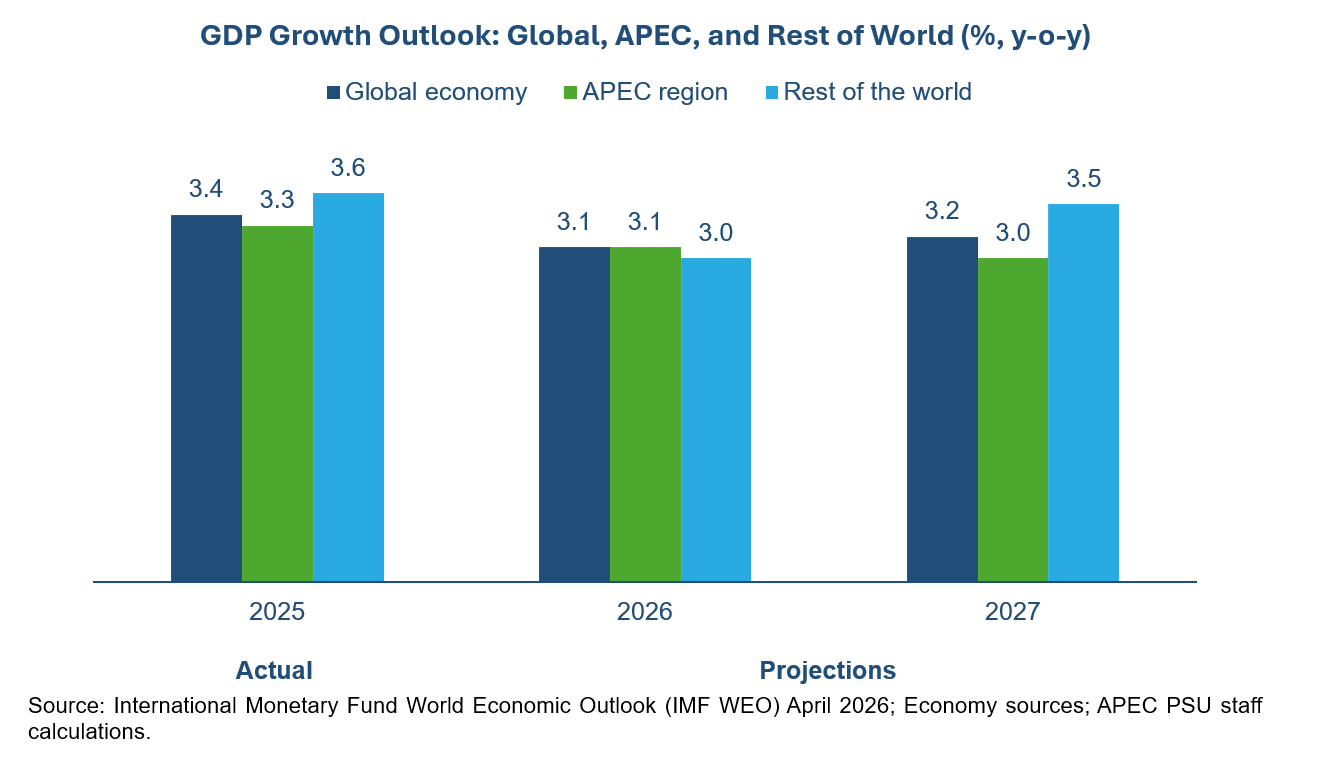

APEC’s GDP expanded by 3.3 percent in 2025, slightly exceeding projections in the ARTA February 2026, and is expected to moderate marginally to 3.1 percent in 2026 and 3.0 percent in 2027. Over the medium term, however, growth is projected to ease further to 2.7 percent.

This trajectory reflects not a sudden downturn, but a gradual loss of momentum as the adverse effects of multiple shocks brought about by geopolitical tensions, supply disruptions and policy uncertainty begin to accumulate. Future growth scenarios may be adjusted depending on the duration of the current crisis in the Middle East.

Supply disruptions affect inflation and trade

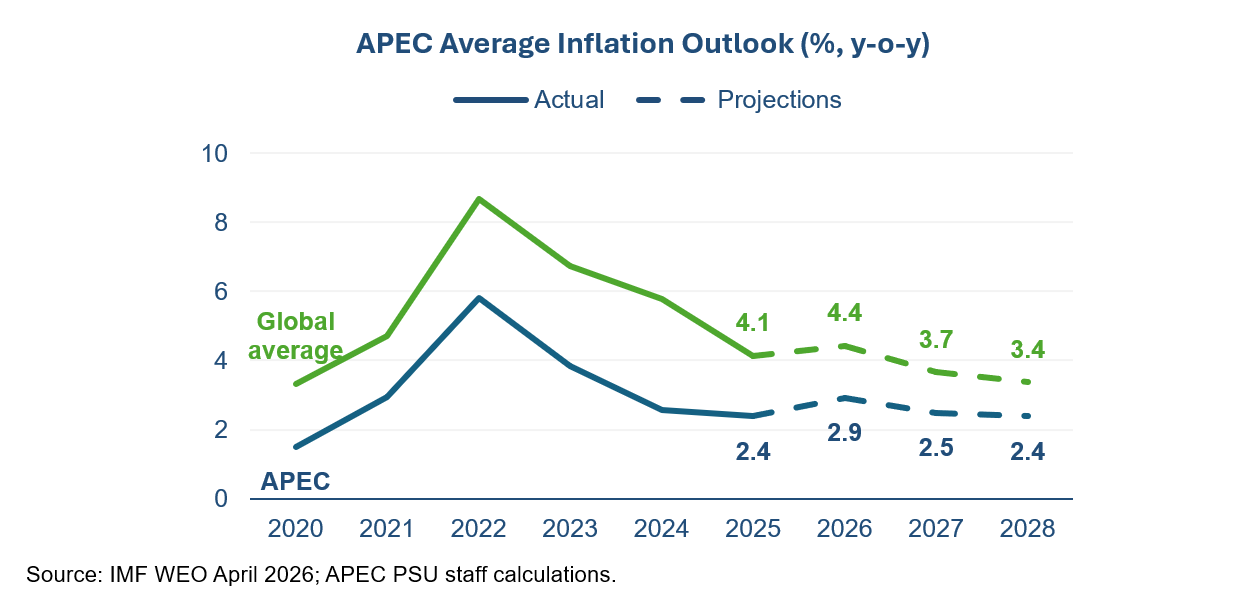

Inflation, meanwhile, is expected to rise to 2.9 percent in 2026, driven in large part by surging energy and food prices, before easing back to around 2.4–2.5 percent from 2027 onward.

At the center of current risks is sharp escalation in energy costs. Average crude oil prices surged by 52.8 percent between February and April 2026, from USD68.0 to USD103.9 per barrel, while liquefied natural gas (LNG) prices rose by 9.3 percent over the same period.

APEC’s heavy reliance on energy imports from the Middle East, which supplies 46 percent of its crude oil and 23 percent of its LNG, leaves the region vulnerable to macroeconomic risks during periods of market turbulence.

Disruptions in the Strait of Hormuz have not only constrained oil flows but also affected critical inputs such as natural gas and fertilizers, amplifying risks to industrial production and food security. Indeed, food prices have already begun to edge upward, particularly for vegetable oils, meat and cereals.

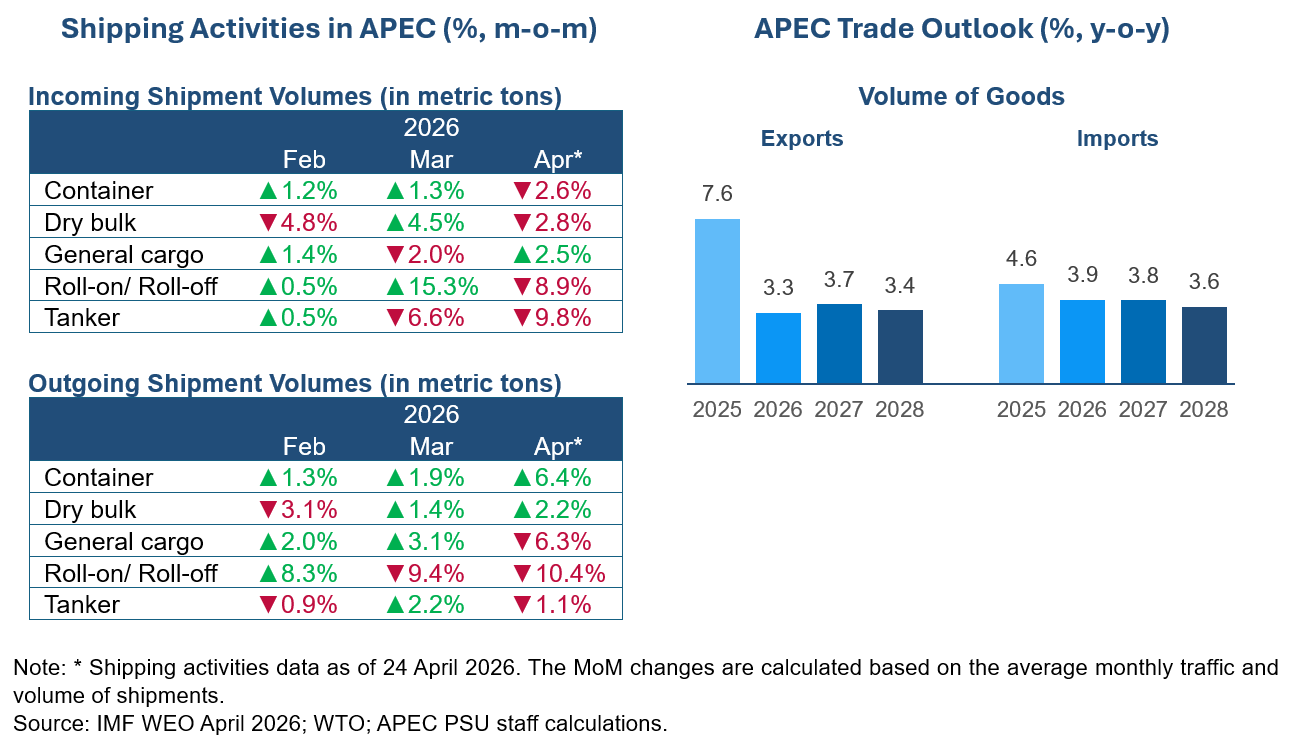

These pressures are reverberating through trade and supply chains. Freight costs are rising across intra-APEC routes, following earlier increases in extra-regional shipping, as higher fuel prices and logistical bottlenecks take hold.

At the same time, port traffic across the region is beginning to decline, with a noticeable divergence between inbound and outbound volumes, an early sign of weakening trade flows. As a result, the near-term outlook points to a slowdown in trade activity, with growth in the volume of merchandise exports projected to moderate to 3.3-3.7 percent between 2006 and 2008.

This marks a shift from the strong performance seen in 2025 when the volume of merchandise exports grew by 7.6 percent, supported by robust demand for high-tech goods and front-loaded shipments amid evolving trade policies. However, this momentum is fading.

Growth in commercial services trade has softened as travel and transport sectors decelerate, while goods-related services now play a larger role. At the same time, an uptick in trade-restrictive measures and trade remedies, particularly tariffs and anti-dumping actions, signals increasing fragmentation in the global trading system.

The imperative of rebalancing

Beyond cyclical pressures, structural challenges are also becoming more pronounced. The region continues to face widening imbalances, reflected in persistent current account surpluses and deficits, with APEC’s aggregate imbalance expected to remain elevated in the near term.

Addressing this issue requires domestic macroeconomic adjustments, including strengthening demand in surplus economies and improving competitiveness as well as fiscal and investment efficiency in those recording deficits, rather than resorting to protectionist measures that risk deepening fragmentation.

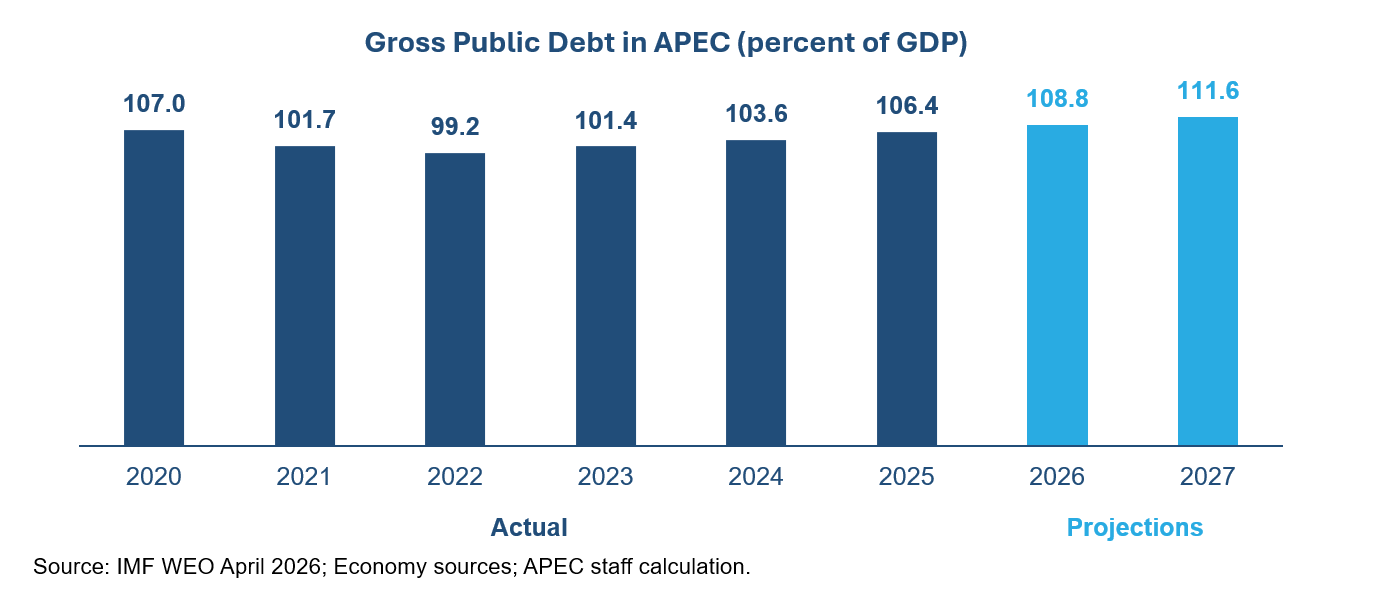

Compounding these risks is the steady rise in public debt. Gross public debt in APEC reached 106percent of GDP in 2025 and is projected to climb to 112 percent by 2027. Elevated debt levels could constrain governments’ ability to respond to future shocks, particularly if financial conditions tighten or growth slows more sharply than expected.

Policy priorities amid shared challenges

Taken together, these developments point to a risk environment where downside factors clearly dominate. The combination of geopolitical tensions, energy price shocks, trade uncertainties and supply chain disruptions is likely to weigh on economic activity well into the medium term.

Yet, there are also sources of resilience. Many APEC economies maintain relatively strong macroeconomic fundamentals and the region has demonstrated agility in diversifying supply chains and sustaining investment in high-tech sectors.

Navigating this complex landscape will require a focused and forward-looking policy response.

First, economies should optimize supply chains by broadening sources, routes and services strengthening logistics connectivity and leveraging digital platforms to enhance transparency and efficiency. For example, in response to current disruptions, some APEC economies are implementing or considering agreements to secure the supply of essential goods.

Second, reducing dependence on volatile energy imports is critical; this means diversifying energy sources, investing in renewables as well as safeguarding and upgrading energy infrastructure.

Third, policymakers must adopt a disciplined fiscal approach, prioritizing high-impact investments while delivering targeted support to households and businesses with significant exposure to economic shocks.

Finally, deeper regional cooperation remains essential. Strengthening coordination within APEC can help economies move beyond short-term resilience toward future-readiness, enabling the region to better withstand shared shocks and sustain growth that benefits all people.

Amid heightened uncertainty, APEC’s challenge is no longer simply to remain resilient, but to turn resilience into a foundation for stability, adaptability and sustained prosperity.

Rhea Crisologo Hernando is analyst, Eldo Simanjuntak is researcher and Carlos Kuriyama is director at the APEC Policy Support Unit.

For more on this topic, download the latest APEC Regional Trends Analysis report.